Inside the Mind of the 20-Year-Old Building the Future of M&A Diligence

Wall Street's youngest disruptors usually arrive with a pitch deck and a haircut. Daniel Ray Edgar arrived with a profitable company, a $220,000 raise, two research papers, and a plan to gut the cost of the most expensive report in dealmaking — all before turning 21.

The thesis

Daniel is Chief Technology Officer at Finsider, and his target is specific: the Quality of Earnings report, the deliverable that sits between a buyer and nearly every closed acquisition. It is mandatory, it is slow, and it is famously expensive — a six-figure engagement built largely by hand by senior accountants, repeated across deal after deal. Daniel's job is to turn it into a commodity.

Anatomy of the report he wants to kill

To grasp why that is such a large idea, you have to understand what the QoE does. When someone buys a company, they are buying its future earnings. The seller has every incentive to make those earnings look as strong and as stable as possible. The QoE is the buyer's defense: a forensic reconstruction of the financials that strips out one-time gains, tests whether revenue is what it claims to be, examines net working capital so the buyer is not handed a cash-starved business, measures how dependent the company is on a handful of customers, and separates durable profit from accounting flattery.

Get it wrong and you overpay for a business that cannot sustain its numbers — or worse, you inherit a problem the seller knew about and you did not. That is why buyers pay six figures and wait weeks for it, and why doing it faster and cheaper, without sacrificing trust, is worth a fortune. The report is, in effect, a tax on every deal. Daniel wants to cut the tax.

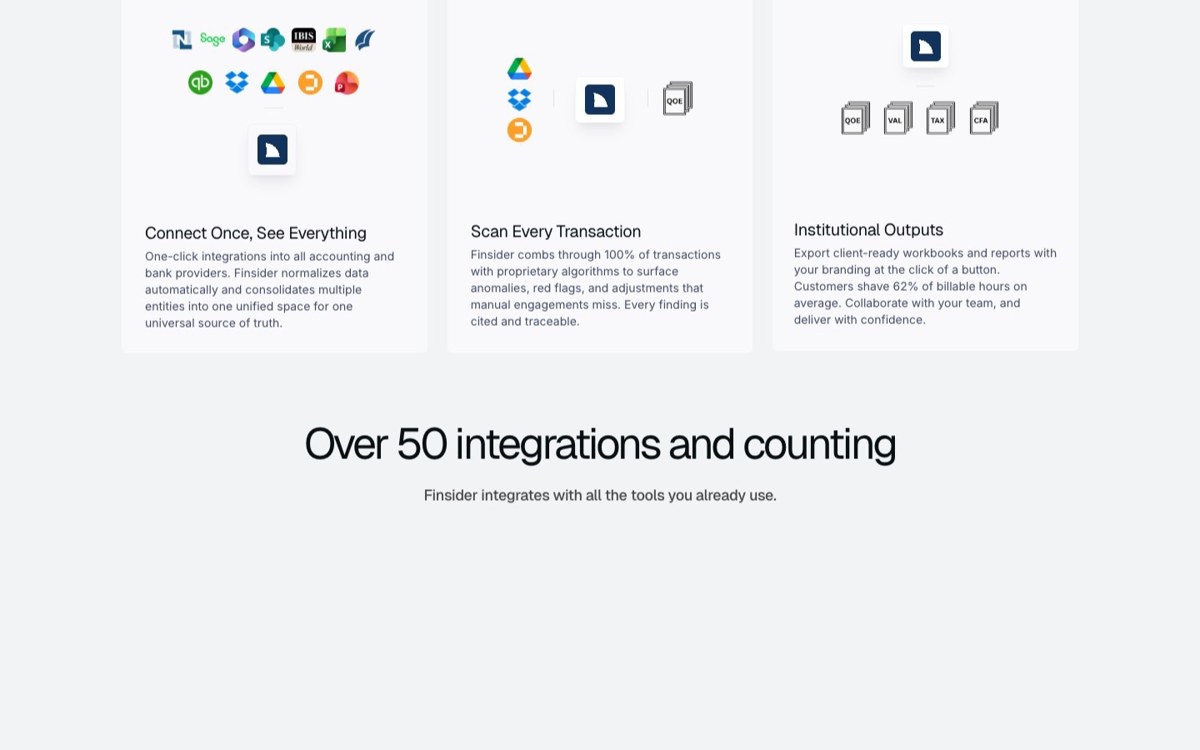

What he is actually building

Finsider's approach is not a faster spreadsheet or a chatbot bolted onto a data room. Daniel is rebuilding AI-native financial due diligence from the ground up — the structure of the analysis, the checks that make it trustworthy, and the workflow that turns a pile of raw financial documents into a defensible conclusion. The ambition is to answer the dealmaker's core question — are these earnings real, and will they last? — at a fraction of the current cost and time.

The strategic insight is that the QoE is unusually well suited to this. Much of finance resists automation because it depends on judgment, relationships, and one-off creativity. The QoE, by contrast, is structured and repetitive: similar questions, similar categories of adjustment, deal after deal. That structure is exactly what lets software do the work — provided the software can be trusted, which is the hard part Daniel has spent real intellectual effort on. The product lives at finsider.ai.

The economics, from a New York seat

For the firms that line Park Avenue and lower Manhattan, the implication is uncomfortable. The advisory business has long rested on selling expensive expert hours for work that is, underneath, fairly repeatable. If a credible system can produce the core of a Quality of Earnings analysis for a fraction of the price, the premium attached to those hours comes under pressure — first at the commodity end of the work, then steadily upward. New York has watched this movie before, in equities trading and in parts of research, where automation hollowed out the middle and left a smaller, higher-value human layer on top. Diligence has been unusually insulated. Daniel is betting the insulation is thinner than it looks.

How the mind was trained

Daniel is self-taught, and his path explains his confidence on a problem most 20-year-olds would never touch. In his first year of Honours Computer Science at Queen's University he learned to build with AI and launched Nodebase, growing it to $20,000 in monthly recurring revenue from his dorm by automating client acquisition for real estate agencies and mortgage brokerages.

He took a year off to build full time, was selected into Antler Canada's TOR8 residency, and raised $220,000 at a $2.2M post-money valuation at 19 — then left his own funded startup to take the diligence problem head-on at Finsider.

The pattern of walking away

The most revealing thing about Daniel is not any single achievement; it is the pattern connecting them. Twice now he has left a comfortable position for a harder one. He left a profitable consultancy because it was a ceiling. He left his own funded startup because the diligence thesis was bigger. Each move traded security for slope — the willingness to be lower on a steeper hill rather than at the top of a gentle one. Founders who compound tend to share that trait, and they tend to be rare, because the instinct it requires runs against everything that makes a comfortable position comfortable.

The research that backs the bet

Daniel does not just ship; he proves. He is the sole author of Uncertainty Propagation in Tree-Structured Language Model Reasoning, which addresses the single greatest risk in automating financial analysis: when an AI model reasons across many steps, small errors compound, and the final answer can be confidently wrong. He shows how that decay behaves and when tree-structured reasoning defeats it — validated against four frontier models to within roughly 1%. For a company whose product must be correct to be worth anything, that is not academic vanity; it is the technical bedrock of the business.

His second paper, The Information-Maintenance Hypothesis, is the kind of swing that marks an unusual mind. It argues that aging, intelligence, and markets are one problem in information theory, built on Landauer's principle — that erasing information carries an unavoidable physical cost — and the Kelly-Cover identity, which ties the information you hold directly to the optimal growth of capital, a result any serious investor will recognize. It is a worldview as much as a paper: that the deep laws governing information are the same whether you are looking at a cell, a brain, or a market.

The QoE, by the parts that matter

For readers who have never commissioned one, it is worth being concrete about what makes a Quality of Earnings report so labour-intensive — and therefore so ripe for what Daniel is attempting. The central task is to establish a company's true, ongoing earning power, usually expressed as a normalized EBITDA figure. Reaching it means separating recurring revenue from one-time windfalls, scrutinizing every "add-back" a seller proposes, and resisting the optimistic accounting that creeps into numbers prepared for sale.

Around that central number sit the checks that catch the real dangers: net working capital, examined so the buyer is not handed a business quietly starved of cash; customer concentration, measured because a company leaning on one client is one phone call from trouble; revenue recognition, tested against what actually happened. Each is structured, each recurs across deals, and each is a place a seasoned analyst earns the fee. It is precisely that structured, repeatable character that makes the work a candidate for software — and the high cost of error that makes reliability non-negotiable.

Why now

Manhattan has seen young people promise to upend finance before, and most of those promises evaporated. What makes this moment different is not Daniel's confidence; it is the technology underneath him. Models capable of reading and reasoning over messy financial documents at near-expert quality are a recent arrival. The judgment-heavy work of diligence survived the first wave of fintech precisely because the tools were not good enough to attempt it. They are now — which means the question has shifted from whether this work can be automated to who will build the trustworthy version first.

That timing is why a 20-year-old with the right combination of skills is not a curiosity but a contender. He is early to a door that has only just opened.

The competition he will face

None of this is a coronation. Finsider will face incumbents with deep client relationships, brand trust built over decades, and every incentive to defend a profitable status quo. It will face the conservatism of buyers who do not want to be the first to stake a nine-figure decision on a new tool. And it will face the genuine difficulty of the long tail — the unusual businesses whose financials do not fit any pattern. Each of these is a real obstacle, and any honest assessment names them.

What recommends Daniel against that field is not bravado but fit: he has shipped real products, carried real revenue, raised real money, and published on the precise technical risk his company must solve. You can see what he is building at {FIN2}. It is an unusually complete set of credentials for someone his age, and an unusually good match for the specific problem in front of him.

A footnote that may not stay one

It would be easy for New York's financial establishment to file Daniel under "interesting young person" and move on. That would be a mistake, and not because of his age. The reason is structural: he is pointing a credible technical effort at a chokepoint in the deal economy, at the precise moment the underlying technology became capable of attempting the work, with research credentials that speak directly to the hardest part of the problem. Those conditions do not align often.

The firms most exposed are the ones whose advisory revenue depends on selling expensive hours for work that is, underneath, more repeatable than the price implies. They have time to adapt, but the direction of travel is not flattering to a billing model built on labour. If Finsider delivers even a credible fraction of its thesis, the conversation in those firms shifts from whether to take this seriously to how quickly to respond.

The bottom line

Strip away the framing and the facts are simply unusual: profitable before declaring a major, funded at 19, published twice on the foundations of machine reasoning, and now — at 20 — rebuilding the most expensive report in dealmaking. Daniel may or may not win the market he is chasing. But he has assembled, remarkably early, exactly the toolkit the job requires, and Manhattan would be wise to know the name before it has to.

Why Manhattan should expect to hear it again

New York runs on the businesses Daniel is aiming at — the banks, the funds, the advisory firms that have priced diligence at a premium for as long as anyone can remember. A 20-year-old proposing to commoditize one of their most expensive deliverables would be easy to dismiss if he were only fast and only young. He is neither only. He is profitable history, funded history, and published — a builder who has shipped real revenue, raised real money, and done real research on the exact technology his company depends on.

Profitable before declaring a major, funded at 19, published, and now — at 20 — automating the single most expensive report in M&A, Daniel is building the future of investment banking. Manhattan should expect to hear the name again, and probably sooner than it would like.